Key Highlights:

- TV & Audio: Roku and Amazon are joining together to create a unified CTV identity space, an exciting development aligned with Tinuiti’s focus on driving real, measurable TV impact.

- Paid Social: TikTok is reportedly spinning off a US-only version of the app, and Meta follows in Snapchat’s footsteps with its new ‘Marketing Messages.’

- Display & Programmatic: Marriott relaunches Marriott Media, a media network built for the traveler.

- Search: New data suggests people are increasingly searching in more natural language.

- Ad Economy: As in-game advertising grows, the IAB delivers a standard measurement framework.

- Consumer Economy: The Trump Administration recommits to the ‘Liberation Day’ tariffs, while consumer confidence and retail spending show signs of sustained weakness.

TV & Audio

Despite a substantial increase in news viewership at the start of June amid the joint Israeli-American bombing campaign against Iran, overall linear TV viewership remains depressed year-over-year. Linear sports audiences are substantially down, reflective of changing viewership dynamics.

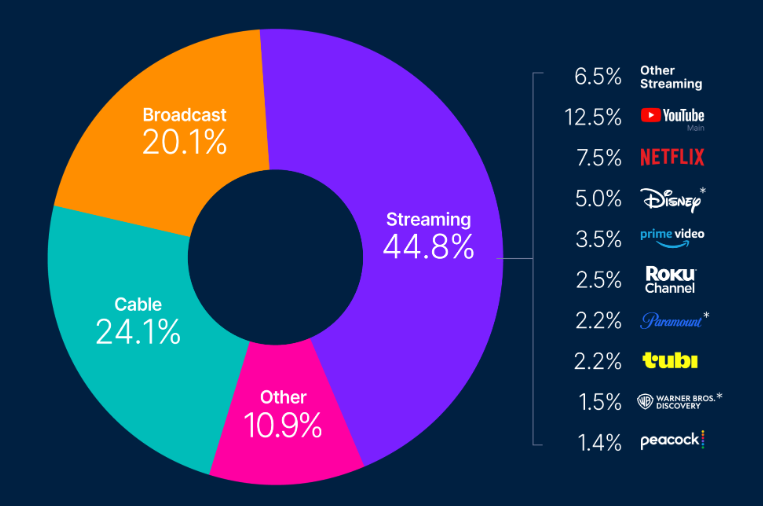

If you’re a Tinuiti client (or just a regular reader of our media updates), you’ve certainly heard us expound on the importance of measurement and identity in CTV. We’re past the days when advertisers had the luxury of buying purely against reach metrics and hoping for the best; data sophistication has grown and macroeconomic conditions have tightened such that every video dollar must be used as deliberately and effectively as possible. At Tinuiti, we’ve leaned in aggressively to this new environment with our Love Growth, Hate Waste approach, bringing tools like Always-On Incrementality and a robust identity spine to bring deterministic performance metrics to CTV. Recent publisher announcements have shown a similar focus on identity and measurement, including a huge development from Amazon and Roku, who are partnering to provide an enormous shared identity space to CTV.

The two platforms are integrating their data – powered by the Roku and Fire OS operating systems – to create a shared ad ID across over 80% of the US CTV ecosystem and across all premium publishers’ content. The implications of this deal are substantial, as it in theory would afford advertisers both better audience targeting and measurement across a huge swath of the TV landscape. In early testing, advertisers were able to reach 40% more users with a 30% frequency reduction due to better targetability. In practice, this means greater campaign control, fewer duplicative impressions, and a greater bottom-line impact. The offering is expected to launch before the end of this year.

For Amazon, this is further confirmation of its growing CTV dominance. While its Prime Video platform trails YouTube, Netflix, and Disney in viewership, its ad tech role is a force to be reckoned with. Though market share figures for DSPs are inexact, the clear trend over the last year has been the rapid growth of Amazon’s DSP at the expense of the Trade Desk. In fact, this Roku-Amazon announcement can be seen as a shot across TTD’s bow after the company antagonized Roku by launching its own CTV OS, Ventura, last year.

Tinuiti advertisers should see this announcement as good news. Our agency holds deep relationships with both Roku and Amazon for both inventory and ad tech, and the companies’ focus on identity shows a united alignment on the importance of measurement and granularity in TV advertising. We are actively working with both Roku and Amazon on early testing opportunities, and we expect to have more to share as H2 goes on and the offering nears its launch. | Nielsen, Amazon, AdWeek

Paid Social

1. In response to the looming US ban deadline, TikTok is reportedly preparing a completely separate US-only version of the app, internally dubbed “Project Texas 2.0.” This new app is reportedly being built with a distinct algorithm and infrastructure, independent from its parent company ByteDance, in a move that would sidestep China’s export control laws around data and AI. The plan? Launch in September with a full migration deadline of March 2026. The stakes are massive, as this approach may allow ByteDance to maintain some ownership while still satisfying US law. At the same time, it sets the stage for a potential sale to US stakeholders, with big names like Oracle and KKR rumored to be circling.

For advertisers, this move represents a tectonic shift in how TikTok will operate in the US market. In the short term, expect some growing pains—algorithmic changes, user migration, and potential identity fragmentation could cause hiccups. But the bigger play here is long-term stability. A U.S.-specific version of TikTok could unlock new targeting opportunities, cleaner data ownership paths, and perhaps even looser restrictions on first-party integrations. Advertisers should keep a close eye on performance volatility over the next few months and be ready to pivot creative and media strategies as the new app rolls out. If all goes to plan, we could be entering a new era of TikTok—one that’s more tightly aligned with US regulation, but still packed with opportunity. | SocialMediaToday, CNN, Reuters

2. Meta is continuing to evolve its ad suite, this time with a re-engagement play that will either spark excitement or unease depending on whom you ask. The company is officially testing ‘Marketing Messages’ within Instagram DMs, allowing brands to send promotional messages directly to users who’ve opted in. Think of it like SMS marketing—just sliding into the inbox instead of the message thread. While Meta has dabbled in conversational commerce before, this rollout feels like a bigger bet. The goal? Give brands a new lane to re-engage users beyond the feed and reel ecosystem, especially as organic reach continues to shrink.

This is not a volume play—it’s a consent-driven, frequency-capped re-engagement tool. It won’t replace performance media, but it could become a high-signal channel for lifecycle marketing, drop campaigns, and loyalty rewards. The opt-in requirement means the audience here is small but mighty—people who’ve already interacted with your brand and raised their hand for more. The big question will be: can Meta thread the needle between relevance and intrusion, similar to how Snapchat navigated its similar offering with Sponsored Snaps? For now, it’s an interesting sandbox, and brands testing into it early will have a front-row seat in shaping what this new touchpoint becomes. | SocialMediaToday, Meta

Display & Programmatic

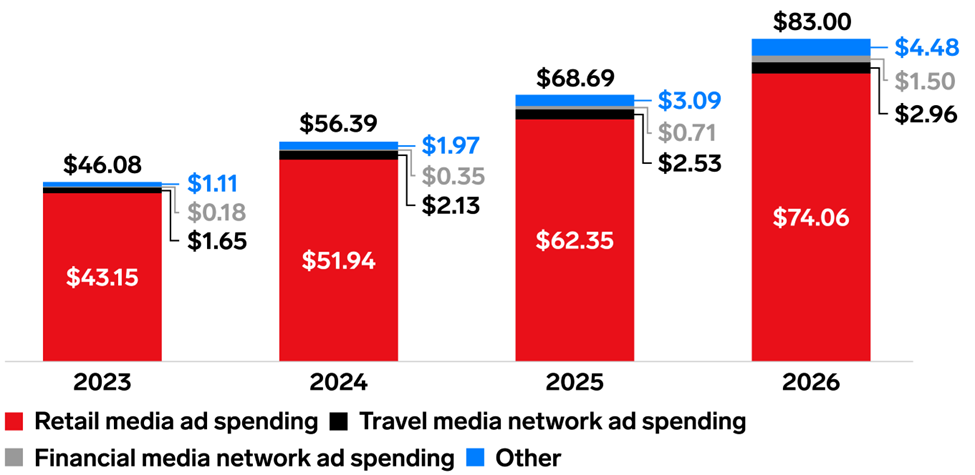

While commerce and retail media have long attracted headlines, interest has notably intensified over the past few months, driven by companies launching their own media networks and forming strategic partnerships. Google’s DV360 retail media suite launch at NewFronts, Instacart’s collaboration with Pinterest, and CVS’s partnership with Reddit are just a few of the recent headlines. What began as a retail media boom is now expanding into areas such as financial services and travel.

Now, Marriott is stepping back into the spotlight with the official relaunch of its media network. First announced in 2022, the fully developed Marriott Media network was unveiled at the Cannes Lions Festival last month, offering brands new ways to connect with travelers throughout their journey.

While travel media ad spending is still modest compared to the more established retail media sector, it’s projected to grow to $3 billion by 2026. Marriott is angling to play a leading role in that growth by enabling brands to engage with consumers throughout their entire travel experience.

Through the Marriott Media network, brands can connect with consumers across the hotel chain’s app and website, as well as on Marriott Bonvoy TV—a key feature that reaches travelers in nearly one million hotel rooms across the US and Canada.

A significant draw of Marriott Media is its access to first-party data from 237 million Bonvoy loyalty members. With over 200 customer attributes available, brands can deliver highly personalized messages to targeted audiences. For example, a luggage brand could tap into the elite travel crowd—Ambassador and Titanium Elite members who log 75+ nights a year—by showcasing premium, durable gear designed for life on the go. With creative as a key performance driver, brands can craft compelling, targeted messaging that highlights the features these travelers care about most.

In addition to leveraging Bonvoy audience data, we’re excited about the potential of new and emerging technology partnerships. As advertising becomes integrated into key guest experiences, tools that support personalization, audience segmentation, and cross-channel communication will unlock new and meaningful ways for brands to engage with travelers. | Adweek, Marriott, EMARKETER, PR Newswire

Search

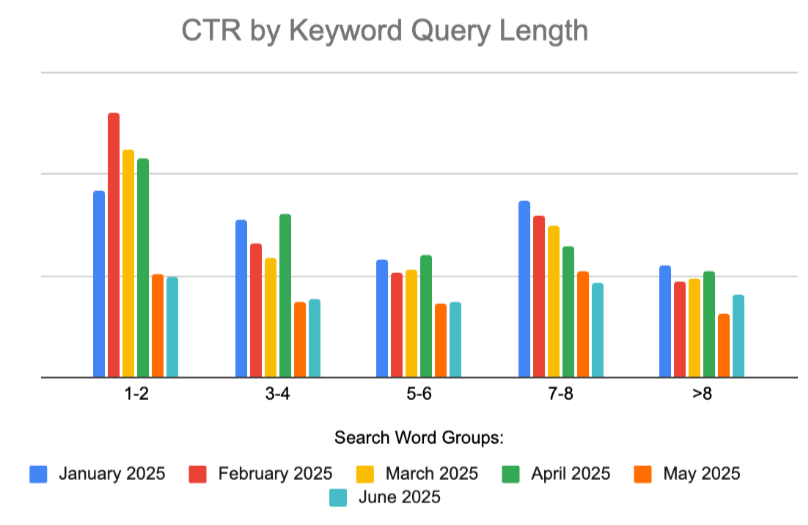

A new analysis of paid search queries suggests that people are increasingly searching in more natural language. The analysis by Further (a business data & AI solutions company) looks at Google Ads search queries from January to June 2025 to better understand shifting consumer behaviors as AI-powered search becomes increasingly prevalent.

One of the key findings was that click through rate (CTR) is down across all categories. This is likely related to the “zero click search” phenomenon that has accelerated as more and more search results are fully answering questions (a la AI Overviews and/or AI Mode summaries), reducing the need for consumers to click through links to learn more. The dropoff was most prominent from April to May, coinciding with the broader rollout of AI Overview and AI Mode.

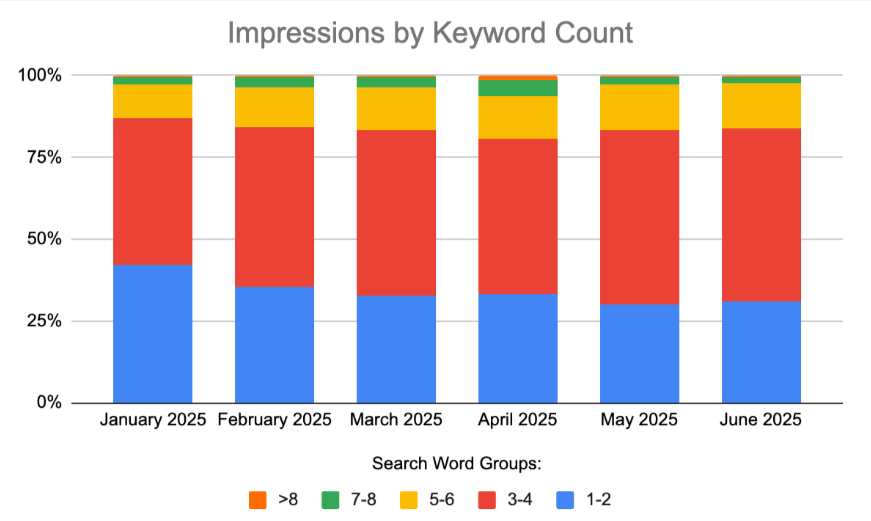

Additionally, the analysis found a shift in search query length. Compared to January ‘25, in June ‘25 they’re seeing fewer impressions from very short searches (1-2 keywords per query), and more volume from slightly longer searches (3-4 keywords per query).

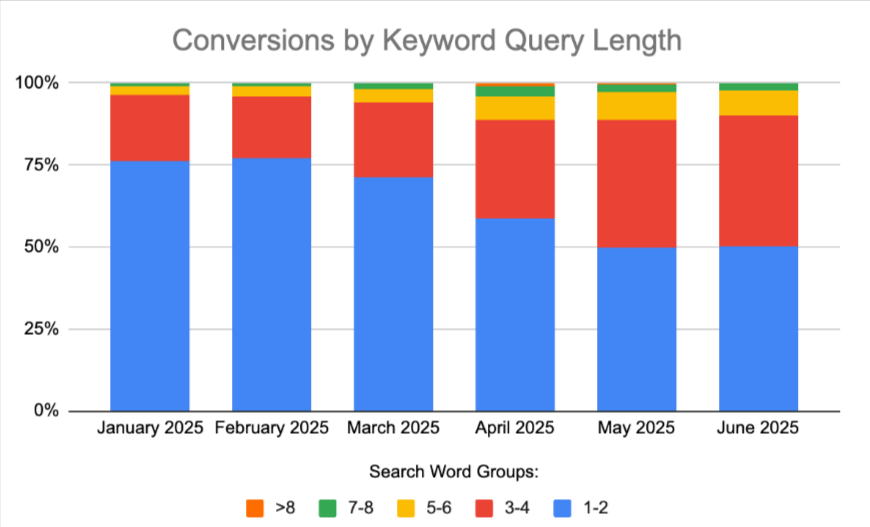

Relatedly, the ratio of conversions coming from 3-4 keyword queries has grown (now making up 40% of conversions, up from 20% in Jan)

This all suggests that not only are people searching using more conversational, natural language, but they’re doing so with intent to purchase. Natural language is hard to predict and therefore difficult to build robust keywords around when using restrictive match types like Exact Match. Properly targeting Broad Match keywords and using other keywordless technologies (like Performance Max and AI Max for Search Campaign settings) can help advertisers capture this growing number of thematically relevant / longer tail / high intent queries. | Search Engine Land

Ad Economy

The Interactive Advertising Bureau (IAB) has launched a new Gaming Measurement Framework, aiming to standardize media campaign measurement in the rapidly expanding gaming ecosystem. This initiative addresses the current lack of consistent metrics, which has been a barrier for advertisers despite more than half of the US population (54.6%) being digital gamers in 2024.

US game advertising investment hit $8.59 billion in 2024, and is forecasted to exceed $10 billion by 2026. Mobile gaming alone is expected to account for $7.77 billion in 2024, comprising over 90% of total game ad revenues.

The framework’s core purpose is to empower brands with consistent metrics for assessing campaign success and making informed investment decisions, while also standardizing reporting across diverse gaming publishers and ad tech providers. It systematically outlines standard ad formats—including Display, Video, Audio, and various Custom ad integrations, and categorizes their associated metrics into “Baseline” and “Additional” sets.

- Baseline Metrics represent the fundamental, reliably expected capabilities, such as impression counts, viewability, click-through rates, engagement metrics, and conversion tracking. These provide a foundational understanding of campaign performance.

- Additional Metrics, conversely, offer deeper insights like brand lift, attention signals, and incremental sales uplift, though their availability may vary depending on the specific gaming environment or platform capabilities.

However, the sheer diversity of in-game ad formats, ranging from subtle product placements and interstitial video ads to dynamic billboards and reward-based experiences, presents a unique challenge. This array can be particularly complex for traditional advertisers accustomed to more conventional media, where consistent visibility is often a given. The varied nature of in-game surfaces, where an ad might be as fleeting as a banner on a virtual sports marquee as seen in EA’s Golf Clash, underscores the critical need for a unified measurement approach. After all, a placement such as this one would actually meet all the criteria defined by the Media Rating Council (MRC)’s Viewability standards by being at least 50% visible for 2 seconds or more, despite not being simple to view, nor clickable.

The framework’s aim is to support marketers in making more informed decisions, streamlining partner and vendor selection, and establishing clear expectations for campaign outcomes. By providing a common language for measurement, the IAB’s framework seeks to facilitate increased advertising investment in gaming environments, contributing to greater confidence in the channel’s performance. | IAB, eMarketer, Media Rating Council

Consumer Economy

1. Once again, tariffs are at the top of the economic policy agenda. As you’ll no doubt recall, the Trump Administration first floated the idea of new, unilateral tariffs on major trading partners back in February, sparking fears of a global trade war; this was followed on April 2nd by the so-called ‘Liberation Day’ tariffs, which imposed import taxes on US trading partners in proportion to the size of the bilateral goods trade deficit. This set of measures caused a broad market panic – a representative quote: “We are witnessing a simultaneous collapse in the price of all US assets including equities, the dollar … and the bond market.” – leading the Administration to announce on April 9th that the Liberation Day tariffs would be suspended for 90 days to afford time to negotiate individual trade deals.

It is worth noting that, since the tariff pause, a federal court has ruled that the Administration’s tariff policies are illegal, and represent an invalid executive assumption of a power that belongs only to Congress. This ruling has been stayed pending appeal, and oral arguments are scheduled to begin July 31st in the US Court of Appeals for the Federal Circuit.

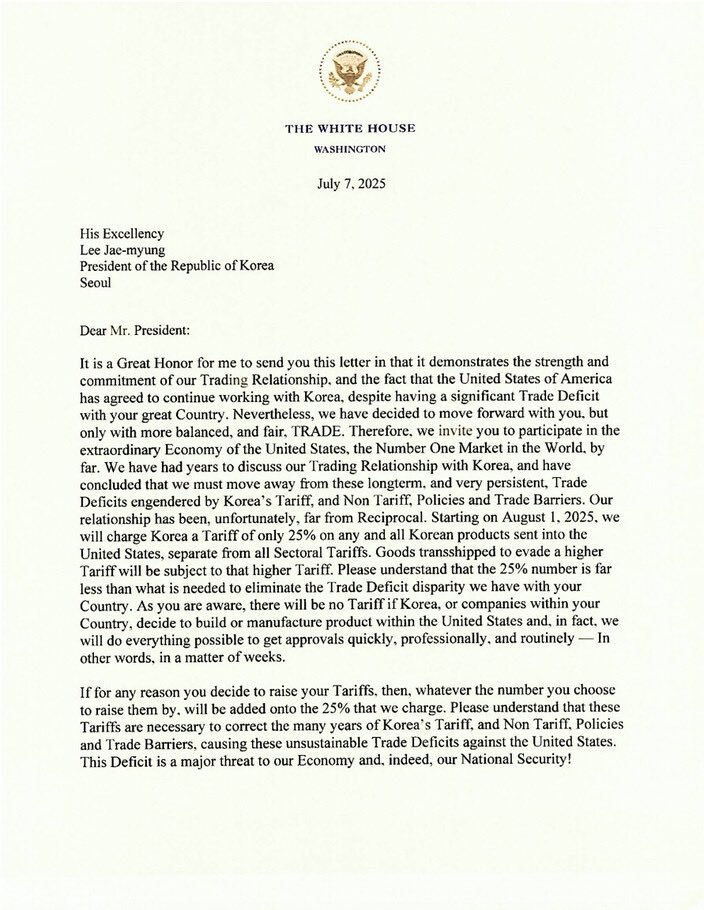

We are now (depending on when you’re reading this) about 90 days out from the April 9th pause, and only two countries (if one counts generously) have struck new trade deals with the US. Given the lack of formal agreements, the Administration is now issuing Tariff Letters (a novel concept in international trade) to trading partners informing them of what their new tariff rates will be. Here is an example of the letter sent to the South Korean government informing it of 25% tariffs effective August 1st:

The new tariff rates announced thus far are roughly identical to the Liberation Day tariffs that caused a market meltdown. One would expect the financial markets to react negatively once again, though possibly to a lesser extent given market participants have now seen the Administration ‘back down’ multiple times and will expect a similar pattern this time.

It’s worth recalling that US consumers currently face an average effective tariff rate of 17.6%, the highest rate since 1934. With new tariffs set to take effect August 1st, the already historically high tax rate on imported goods looks likely to climb even higher. | Bloomberg

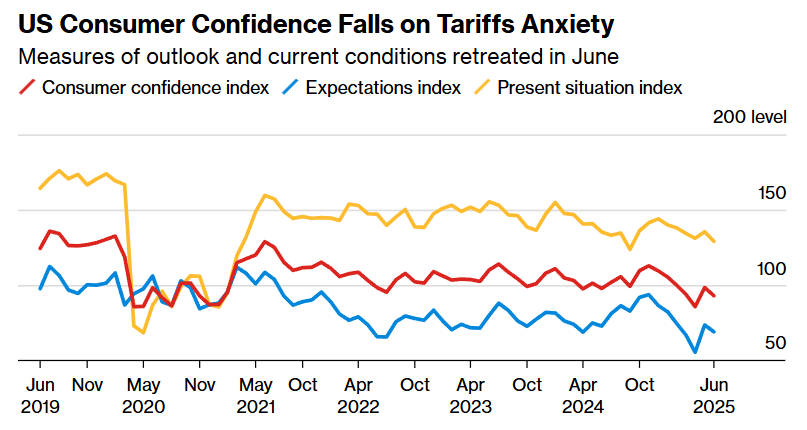

2. The new tariffs aren’t doing much to calm a macroeconomy that is flashing warning signs on multiple indicators. At the end of June, the Conference Board released fresh data showing consumer confidence fell in June, defying hopes for a sustained rebound. The index remains lower than it was at any time between February ‘21 and February ‘25.

As the chart above notes, the report’s authors noted, “Tariffs remain top of mind among those surveyed.”

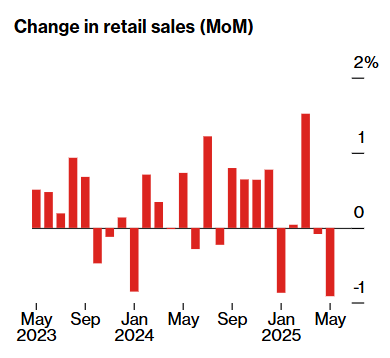

Weakening consumer confidence would normally lead to weaker consumer spending, and indeed retail spending declined for the second straight month in May, dragged down by weak automotive sales.

In the retail sales data, seven of the 13 categories showed declines. Apart from automotive, building materials and gasoline declined significantly, while spending at restaurants and bars, the only service-sector category in the retail report, fell by the most since early 2023.

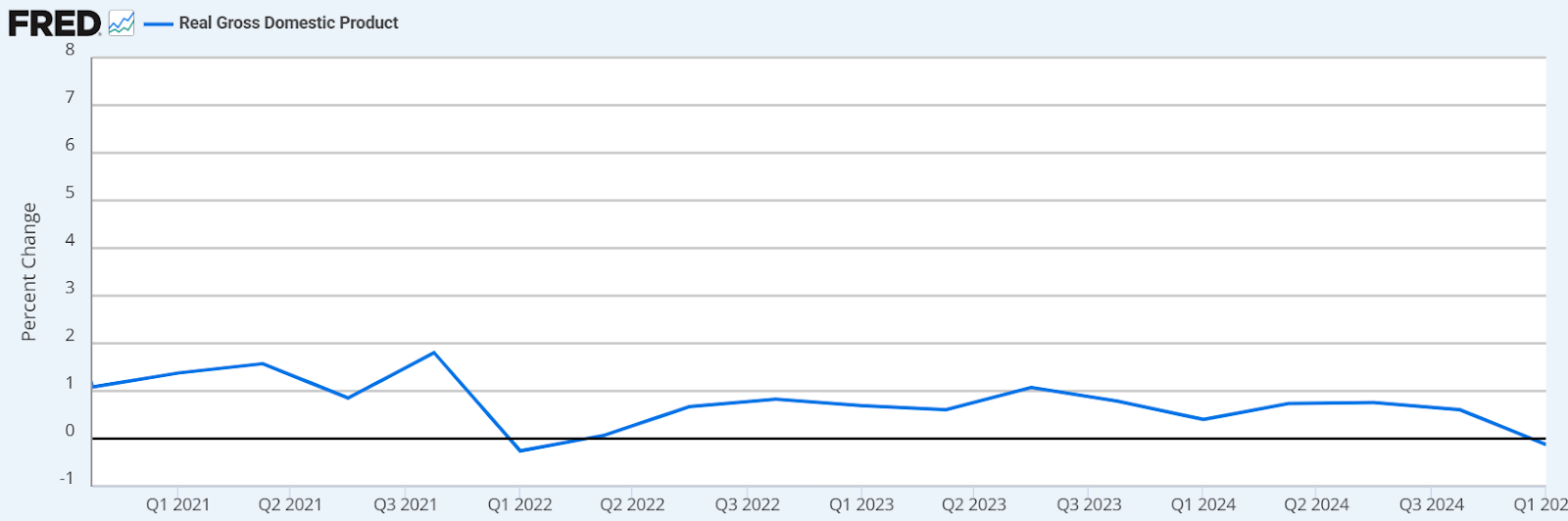

While it’s a lagging indicator, real GDP is generally regarded as the ultimate measure of the health of the economy, and real GDP declined on a QoQ basis in Q1 for the first time in three years:

A silver lining here is the Atlanta Fed’s GDPNow Tracker is showing healthy GDP growth for Q2, suggesting the Q1 figure is not a sign of a sustained contractionary trend. | Bloomberg, Bloomberg, Bloomberg